Curious whether your super balance could buy an investment property? A quick call is the easiest place to start.

Book a quick callIs Using Super to Buy an Investment Property Right for You?

The strategy works best for investors with a reasonable super balance, a long runway to retirement, and a preference for control. Conversely, if your balance is small or you need to access the money soon, the costs and rules may outweigh the benefits.

This is where the homework earns its keep. You want the right property, in a location with genuine rental demand, structured the right way from day one. Get the structure wrong and the tax advantages can unravel, so it pays to take advice before you buy.

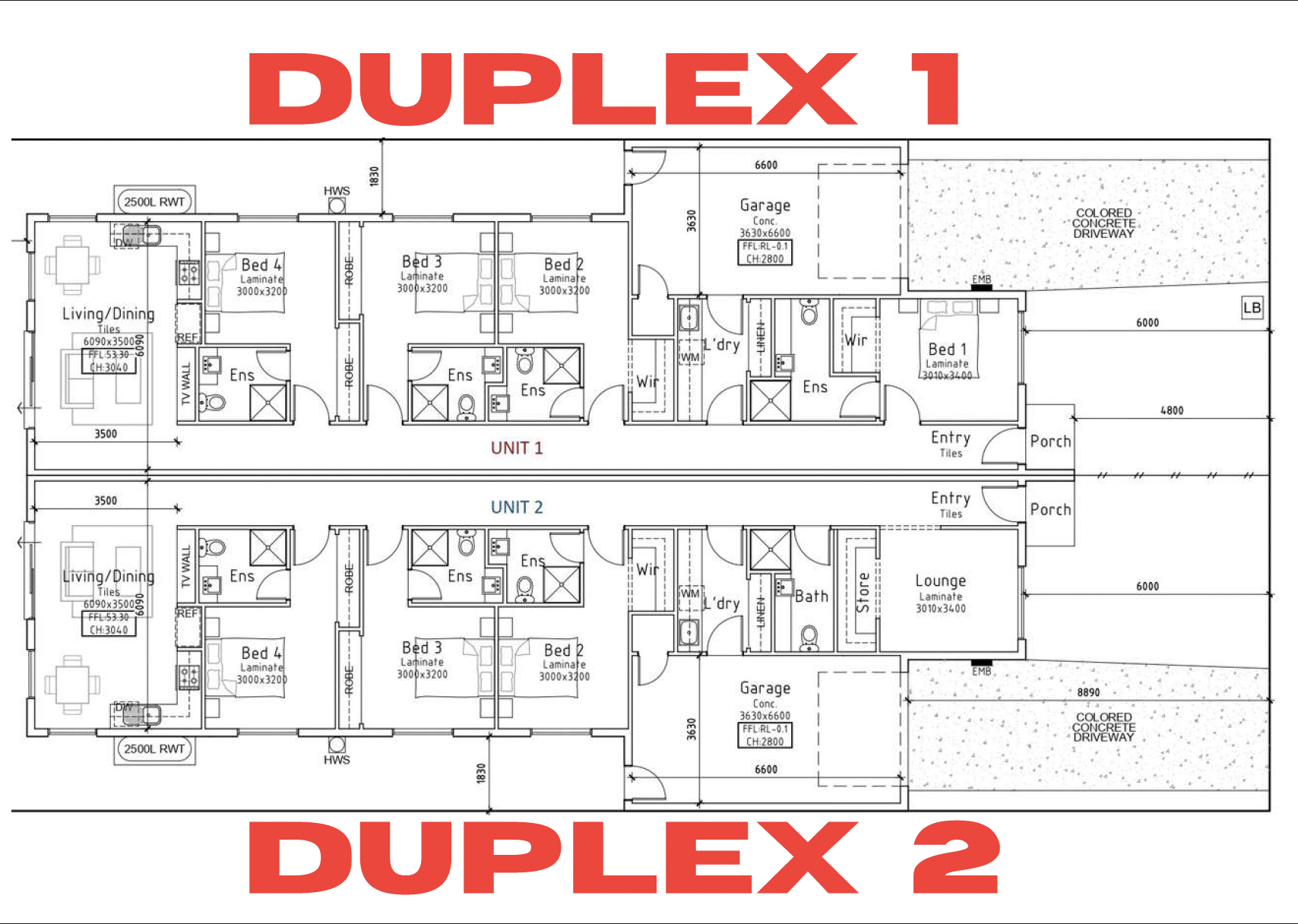

The Properties We Are Recommending Right Now

Right now we are recommending two brand-new half duplexes at Uptown Estate, Shepparton North in regional Victoria, both backed by a 100% 5-year rental guarantee.

Want to see which of these your super could fund? We can walk through the numbers with you, calmly.

Book a quick callSMSF Property Investment FAQs

Can I use my super to buy an investment property?

Yes, but only through a self-managed super fund. An ordinary retail or industry fund cannot buy a direct investment property, whereas an SMSF can buy one and hold it for your retirement.

How much super do I need to buy an investment property?

There is no legal minimum. However, many SMSF lenders look for a fund balance in the ballpark of $200,000 before lending, and they typically want a deposit of around 20 to 30 per cent.

Can I live in a property my SMSF owns?

No. Neither you nor any related party can live in, holiday in, or rent a residential property the fund owns. The fund must run it as a genuine arm’s-length investment.

What are the downsides of buying property with super?

The main trade-offs are higher running costs, strict compliance rules, and limited access to the money until retirement. In return, you gain control and concessional tax treatment inside the fund.

How Positive Income Properties Helps With Buying Property With Super

Positive Income Properties researches and supplies pre-packaged, brand-new investment properties in locations with genuine rental demand. New builds sit squarely inside the category the 2026 proposals protect, which makes them a natural fit for an SMSF. To find where new stock makes sense, we assess employment growth, infrastructure pipelines, population forecasts and rental performance. Our investors gain access to more than 1,600 positive cash flow investment properties, and many return as their portfolios grow.

We do not set up your fund or give tax advice. Instead, we work alongside your accountant and SMSF specialist to find a property that fits the structure. So the smart first move is simple: understand the numbers before you commit.

See whether your super could fund one of these properties. A quick call is the easiest place to start.

Book a quick callTo talk through what using super to buy an investment property could mean for your situation, you can also contact Positive Income Properties on +61 468 037 484 or bookings@positiveincome.com.au.

Book a Quick Call

Pick a time that suits and we will talk through the numbers with you, calmly.

Disclaimer: This article is general information only. It is not tax, legal or financial advice. SMSF rules are complex and set by the Australian Taxation Office; getting the structure wrong can have serious tax consequences. Return, yield and rental figures are estimates, not guarantees, and depend on market conditions. The 2026 Budget measures referenced are proposed and not yet law; detail and timing may change. Positive Income Properties is not a financial adviser. Please seek independent legal, financial and taxation advice before setting up an SMSF or making any investment decision.

Author: Gil Elliott, Managing Director and Founder of Positive Income Properties, with nearly four decades of experience across the real estate and marketing industries.

Gil Elliott is the Managing Director and Founder of Positive Income Properties. Gil has a rich background in business consulting and property investment. All of these he gained in his nearly four decades of experience in the real estate and marketing industries.